{kind=link}

Canadians admit they could save on average $360 more each month and receive $2,280 in 'extra money' annually but lack the discipline to save

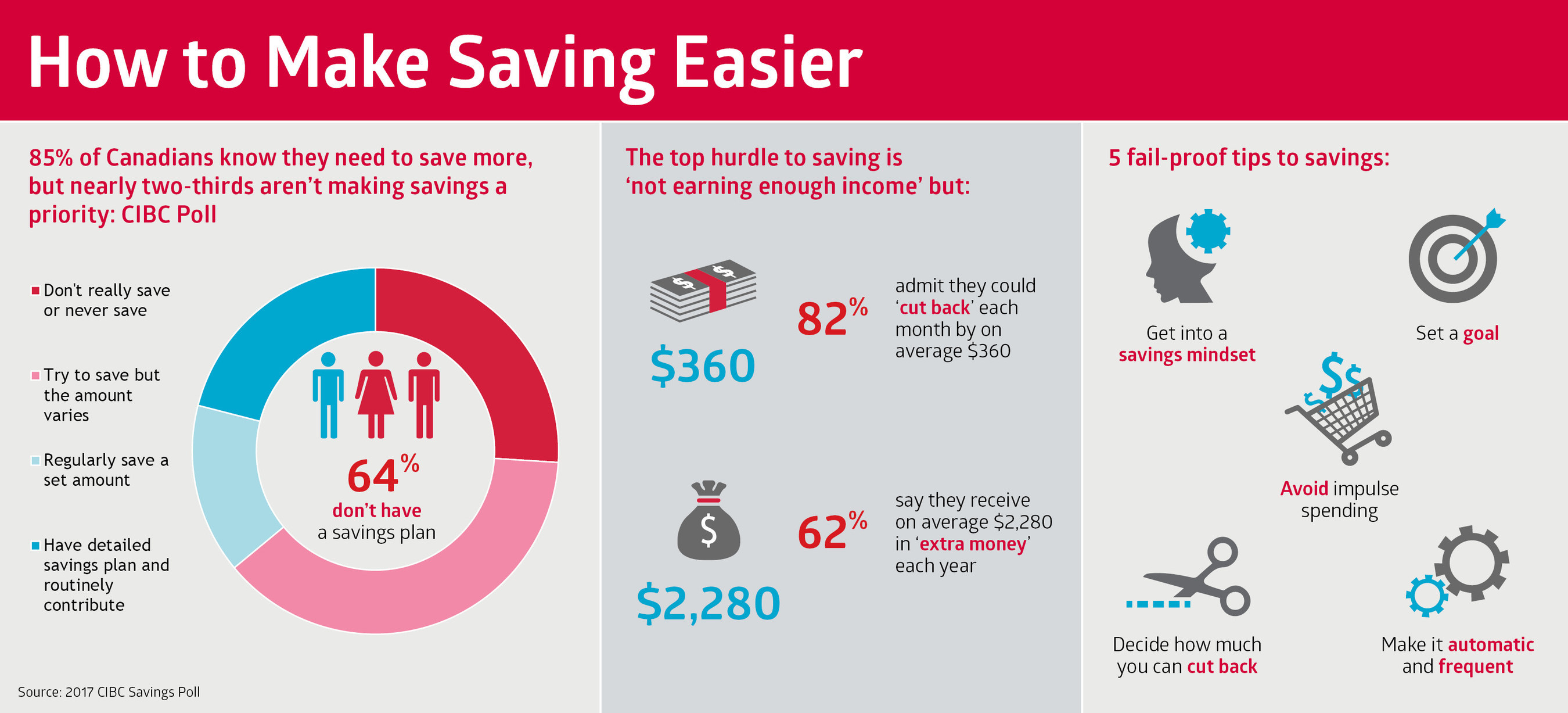

TORONTO, Nov. 21, 2017 /CNW/ - The vast majority (85 per cent) of Canadians agree that they 'need to save more money', but nearly two-thirds (64 per cent) are not making savings a priority, finds a new CIBC (CM:TSX) (CM:NYSE) poll. And, while most admit they could get by with less, few do, and many say 'extra money' is for 'pleasure or enjoyment'.

")

"With consumer spending still strong and fueled by a long period of record low interest rates, the study shows that very few Canadians are making savings a priority, which is concerning as we head into the holiday spending season," says David Nicholson, Vice-President, Imperial Service, CIBC. "This is the time of year when many of us make room in our budget for spending on gifts, Black Friday and Cyber Monday sales and holiday parties, but don't think twice about how little we've saved until regret kicks in with our New Year's resolutions."

Key poll findings:

- 85 per cent of Canadians agree that they 'need to save more money'

- 64 per cent say they lack a detailed or regular savings plan, including 26 per cent who 'don't really save' or 'never save' at all

- 82 per cent admit they could 'cut back' each month by on average $360 'before feeling the pinch'

- In addition to their regular income, nearly two-thirds (62 per cent) say they receive on average $2,280 in 'extra money' each year

- 79 per cent of those aged 35-54 worry about not having enough money to retire when they want to

- 53 per cent of Canadians say they'd use credit or borrow from friends and family if faced with unexpected $1,000 expense

- Top hurdles to saving are: not earning enough income (46 per cent), getting derailed by unexpected expenses (29 per cent), and struggling to pay everyday expenses (24 per cent)

"People think it's too hard to save, but the truth is that we've just become rusty at saving. It's about shifting your mindset, and getting into the habit of saving regularly," says Mr. Nicholson. "The hard part is exercising self-control over your spending so that you can increase the amount you save over time."

No more excuses

A majority of Canadians (82 per cent) admit they could spend, or get by with, less each month -- on average $360 less -- before feeling the pinch.

Further, almost two-thirds (62 per cent) receive 'extra money' each year -- roughly $2,300 on average and as much as $13,100 in the form of cash gifts, employer bonuses, and tax refunds. But, less than half (44 per cent) will save the surplus funds, and two in five say the 'extra money is for pleasure or enjoyment.'

Among those who receive extra cash throughout the year, most (66 per cent) use it to buy themselves gifts, pay everyday expenses, or to chip away at consumer debt. Only two in five (41 per cent) will put those extra funds aside for an emergency, or to boost retirement savings.

With interest rates expected to edge higher and people living longer in retirement, Canadians need to do more than simply spend less, says Mr. Nicholson.

"The real question is, how can you afford not to save? Every day that you delay starting a savings plan, the harder and more expensive it gets to meet your goals later on in life," he says. "The sooner you start a savings plan the sooner your money can be put to work for you."

'Give to' yourself first

The poll findings show that simple saving habits work best, with more than half (55 per cent) of Canadians agreeing they'd be more likely to save if a set sum went automatically off their pay and directly into a dedicated savings account.

"Paying yourself first is an easy and effective savings strategy," says Mr. Nicholson. "For most people, it's actually easier to start with a savings goal first, set an automatic savings plan to meet that goal, and then, simply spend what's leftover."

Having a budget and financial plan helps determine the right savings amount based on each of your short- and long-term goals and monthly cash flow. By setting up the withdrawal on payday, we remove the temptation to spend those dollars, rather than trying to overcome it, he adds.

Directing money into a Tax-Free Savings Account (TFSA) can give an added boost to your savings since the interest or investment income that's earned will be tax-free, helping your money grow faster. Money in a TFSA can also be withdrawn without penalty and used for multiple short- or long-term savings goals, such as to buy a car, renovate your home, take a vacation, tap it for an emergency, or save it for retirement.

"Before you get ready for the first big shopping weekend of the season, think twice and put yourself at the top of the gift-giving list," says Mr. Nicholson. "We automate our bill payments, why not automate our savings? It can help you get through the upcoming season confidently, and get your savings on track."

5 hacks for fail-proof savings:

- Get into a savings mindset

- Set a goal

- Decide how much you can cut back

- Make it automatic and frequent

- Keep spending and credit in check

KEY POLL FINDINGS:

How Canadians would describe their saving style:

|

All Canadians |

|

|

I have a detailed savings plan and contribute routinely to meet my short and long term goals |

21 % |

|

I pay myself first with a set amount dedicated to savings, and then budget with the remaining funds |

15 % |

|

I try to save something each month, but the amount varies depending on what is left over after spending |

38 % |

|

I don't really save – any leftover cash 'goes in a jar' |

13 % |

|

I never save |

13 % |

Amount Canadians say they could cut back (on spending or income) each month before 'feeling the pinch':

|

All Canadians |

Male |

Female |

BC |

AB |

MB/SK |

ON |

QC |

ATL |

|

|

Mean/Average |

$360 |

$411 |

$311 |

$419 |

$442 |

$338 |

$354 |

$341 |

$250 |

|

$0 |

18 % |

17 % |

20 % |

19 % |

17 % |

21 % |

17 % |

18 % |

24 % |

|

Less than $100 |

21 % |

18 % |

23 % |

13 % |

21 % |

23 % |

21 % |

22 % |

27 % |

|

$100-$249 |

23 % |

21 % |

26 % |

23 % |

15 % |

21 % |

26 % |

24 % |

25 % |

|

$250-$499 |

18 % |

19 % |

17 % |

22 % |

20 % |

16 % |

16 % |

19 % |

17 % |

|

$500-$999 |

11 % |

14 % |

8 % |

13 % |

14 % |

12 % |

11 % |

10 % |

4 % |

|

$1000+ |

8 % |

11 % |

6 % |

10 % |

14 % |

6 % |

8 % |

7 % |

3 % |

Top five obstacles to saving for Canadians, by age:

|

All Canadians |

|

|

I don't make enough money |

46 % |

|

I often get derailed by unexpected or emergency expenses (ex. Car or home repairs, health expenses) |

29 % |

|

I struggle to pay everyday bills (ex. Utilities, groceries) |

24 % |

|

Low interest rates/low returns on savings |

19 % |

|

I spend too much money on things I don't necessarily need |

17 % |

Average amounts Canadians receive annually in 'extra money' (excluding regular income) among those who receive any of the following sources:

|

All Canadians |

|

|

Bonus from employer |

$554 |

|

A commission |

$146 |

|

A tax refund |

$857 |

|

Cash for birthdays, holidays or special occasions |

$244 |

|

Other |

$479 |

|

Total |

$2,280 |

Average amounts Canadians receive annually in 'extra money' (excluding regular income) among those who receive each of the following sources:

|

Canadians who receive |

|

|

Bonus from employer |

$3,152 |

|

A commission |

$2,908 |

|

A tax refund |

$1,207 |

|

Cash for birthdays, holidays or special occasions |

$495 |

|

Other |

$5,338 |

|

Total |

$13,098 |

Top uses for 'extra money' among Canadians who receive additional funds annually (excluding regular income):

|

All Canadians |

|

|

Spend on everyday bills, consumer debt, gift for myself etc. |

66 % |

|

Save for short-term spending towards vacation, vehicle, new home/renovation, etc. |

44% |

|

Save for long-term goals (emergency fund, children's education, retirement) |

41 % |

|

Other |

6 % |

|

I don't know |

6 % |

About the CIBC Savings Poll:

From October 20th to October 21st, 2017 an online survey was conducted among 1,523 randomly selected Canadian adults who are Angus Reid Forum panellists. The margin of error—which measures sampling variability—is +/- 2.5%, 19 times out of 20. The results have been statistically weighted according to education, age, gender and region (and in Quebec, language) Census data to ensure a sample representative of the entire adult population of Canada. Discrepancies in or between totals are due to rounding.

About CIBC

CIBC is a leading Canadian-based global financial institution with 11 million personal banking, business, public sector and institutional clients. Across Personal and Small Business Banking, Commercial Banking and Wealth Management, and Capital Markets businesses, CIBC offers a full range of advice, solutions and services through its leading digital banking network, and locations across Canada, in the United States and around the world. Ongoing news releases and more information about CIBC can be found at www.cibc.com/ca/media-centre or by following on LinkedIn (www.linkedin.com/company/cibc), Twitter @CIBC, Facebook (www.facebook.com/CIBC) and Instagram @CIBCNow.

SOURCE CIBC