{kind=link}

With 54 per cent of millennial homeowners opting for an income property, CIBC's Jamie Golombek outlines key tax considerations for landlords in a new report

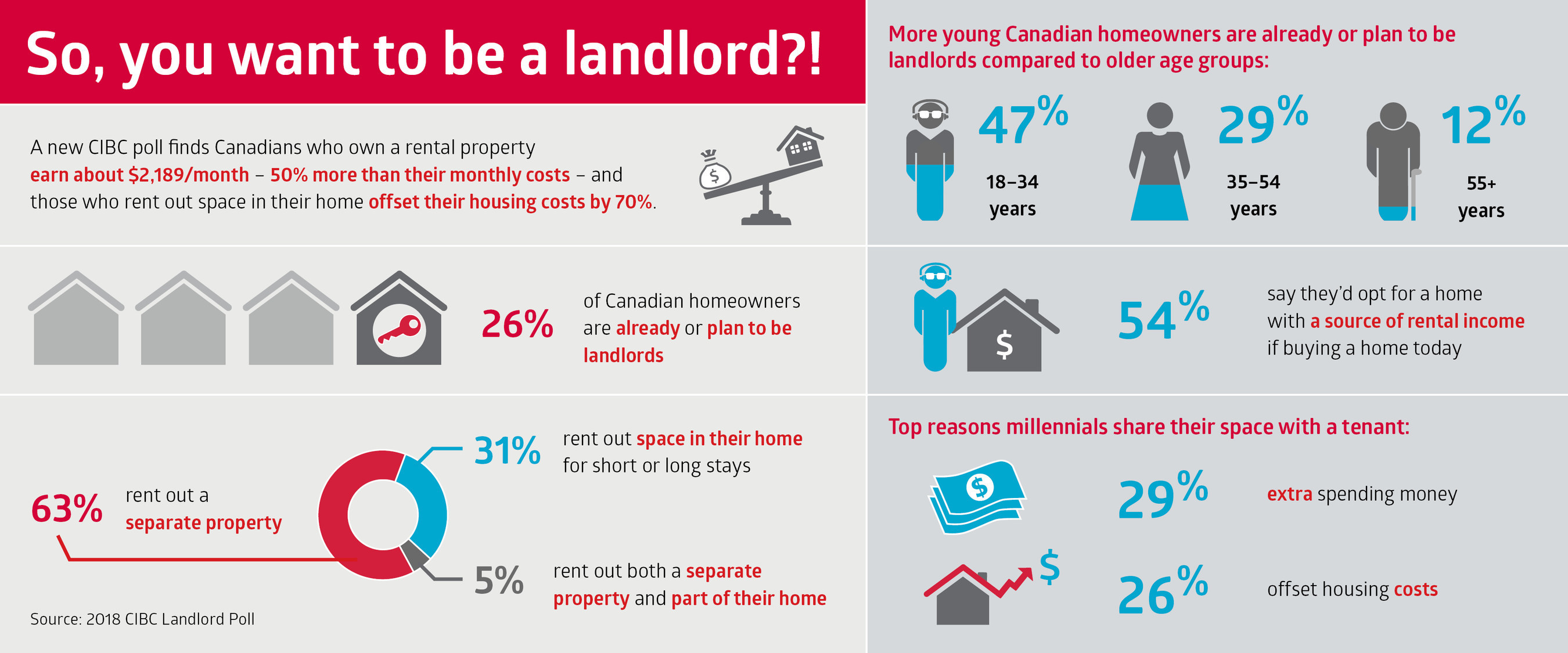

TORONTO, May 17, 2018 /CNW/ - If you think being a landlord isn't worth the trouble, think again. A new CIBC (CM:TSX) (CM:NYSE) poll of Canadian homeowners finds that those who own a separate rental property, earn on average $2,189 per month - 50 per cent more than their monthly costs. Further, those who earn income by renting out space in their home reduce their housing costs by as much as 70 per cent.

")

"High housing costs and the growing appetite for additional revenue streams make renting out space a popular choice, especially among younger Canadians," says Jamie Golombek, Managing Director, Tax and Estate Planning, CIBC Financial Planning and Advice. "While most homeowners believe the tax benefits alone make an income property a worthwhile investment, it's critical to understand how it fits into your overall financial plan, and be mindful of all of the tax implications of going this route so you can make the most of the venture."

In a new report, So, you wanna be a landlord: Tax considerations for rental properties, Mr. Golombek and Debbie Pearl-Weinberg, Executive Director, Tax & Estate Planning, CIBC Financial Planning and Advice, address some of the tax considerations for homeowners currently earning or planning to earn rental income.

Key poll findings:

- More than one in four (26 per cent) Canadian homeowners are already landlords (15 per cent) or plan to earn (11 per cent) rental income by letting out space in their primary residence or from a separate rental property

- Almost two-thirds (64 per cent) of current landlords own one or more investment properties used exclusively for rental income

- $2,189 is the average amount they earn in income each month

- $1,461 is the average amount they spend on expenses each month

- Nearly a third (31 per cent) of current landlords rent out a portion of their primary residence for long-term (22 per cent) or short term stays (9 per cent)

- $1,287 is the average amount they earn in income each month

- $1,888 is the average amount they spend on their total household expenses each month

- 72 per cent of all homeowners believe investing in real estate is an excellent way to earn supplemental income

- 37 per cent of homeowners say they'd opt for a home with a source of rental income if buying a home today

Millennials more apt to be landlords

The poll findings reveal that Canadians aged 18-34 are more apt to be landlords than any other age group. Almost half (47 per cent) of millennial homeowners are already landlords (30 per cent) or plan to be (17 per cent), compared to only 29 per cent of homeowners aged 35-54 and 12 per cent of those aged 55+.

Moreover, if buying a home today, twice as many millennial homeowners than boomers say they'd opt for a home with a source of rental income, at 54 per cent and 25 per cent respectively.

More than half (55 per cent) of millennial landlords own a property exclusively for rental purposes, while 40 per cent rent out a portion of their home for extended stays of a year or more (30 per cent) or short-stays (10 per cent).

Among those who let out a portion of their home, an almost equal number cite additional or surplus income for spending on non-essentials (29 per cent) and to offset mortgage or housing costs (26 per cent) are their top reasons for sharing their space.

"Younger Canadians are more open to sharing their space because they see it as financially advantageous," says Scott McGillivray renowned real estate investor, contractor and television personality. "There's definitely a shift in attitudes and a growing interest in income properties, in part driven by a desire to offset high housing costs, but also because it can be a smart way to create extra income and build wealth."

'Worth the headache'

The survey finds that the majority (80 per cent) of homeowners agree that renting out space in their home makes financial sense, but value their time and privacy too much to pursue it. Further, 30 per cent of landlords say their top concern is dealing with unexpected costs for maintenance and repairs.

Despite this, more than half of landlords (52 per cent) believe it's 'worth the headache.' Among those who own a separate rental property, half say their top reason to invest is to generate passive income now (22 per cent) or in retirement (28 per cent). Another 20 per cent have invested for long-term property appreciation, and only 14 per cent cite future occupancy by themselves or their children as their main reason to invest.

Further, 74 per cent of landlords believe that even with a negative cash flow, the benefits of tax deductions alone make owning an income property a good investment, but Mr. Golombek warns that if expenses exceed income on a consistent basis, you may not be able to claim those deductions.

"Being a landlord can be financially rewarding, but it's not easy money, and would-be landlords often underestimate the taxes they'll pay on rental income and may overestimate what deductions they can claim," says Mr. Golombek. "It's important to be clear on what can and can't lower your overall tax bill."

While landlords who own a separate income property can deduct both capital expenses (e.g. renovations, real estate commissions) over time and current expenses (e.g. insurance, interest) immediately, those who share their primary residence with a tenant can deduct only a portion of their expenses, which relate specifically to the rental area.

The poll also revealed that most (69 per cent) landlords admit they'd discount the rate if renting to family and friends, but Mr. Golombek warns that this could limit the ability to deduct expenses or claim a loss from a tax perspective.

"It's well worth your time up front to consult with a team of experts including your financial advisor, lawyer and realtor to be clear about the perks and perils before jumping in," he adds.

Five tips if considering becoming a landlord:

- Be clear about your income expectations – you'll have to pay tax on rental income and expect to spend 1-2 months of rental income on property maintenance and repairs

- Invest in the location and quality of your space to attract quality tenants

- Understand your legal obligations as a landlord as well as zoning and insurance issues for renting out your space

- Be prepared to spend time and energy addressing tenant concerns promptly

- Stay organized and keep records of all rental expenses

KEY POLL FINDINGS:

Percentage of Canadian homeowners who are landlords, by age:

|

All |

18-34 |

35-54 |

55+ | |

|

I own a residence used exclusively or in part for rental income (e.g. spare room or |

15 % |

30 % |

14 % |

8 % |

|

I don't currently rent out any properties, but I'm thinking about it or plan to do so |

11 % |

17 % |

15 % |

4 % |

|

I do not rent out any of my properties and have no plans to do so |

73 % |

52 % |

71 % |

87 % |

Type of landlord-tenant relationship among Canadian landlords, by age:

|

All |

18-34 |

35-54 |

55+ | |

|

I own one or more investment properties used exclusively for rental income |

64 % |

55 % |

66 % |

65 % |

|

I rent out a portion of my home (primary residence) for long-term rentals (e.g. |

22 % |

30 % |

20 % |

21 % |

|

I rent out a portion of my home (primary residence) for short-term or medium |

9 % |

10 % |

9 % |

9 % |

|

Both – I have an investment property and I also rent out a portion of my home |

5% |

6 % |

5 % |

4 % |

Total amount of expenses per month among landlords, by type of tenant-landlord relationship:

|

All |

Rent out space |

Rent out separate |

Rent out both primary residence | |

|

Average |

$1,615 |

$1,888 |

$1,461 |

$1,910 |

|

< $999 |

28 % |

18 % |

30 % |

22 % |

|

$1,000-$1,999 |

35 % |

34 % |

37 % |

26 % |

|

$2,000-$2,999 |

16 % |

22 % |

13 % |

18 % |

|

$3,000+ |

9 % |

13 % |

7 % |

15 % |

|

I don't know |

13% |

14% |

12% |

19 % |

Total amount of income per month among landlords, by type of tenant-landlord relationship:

|

All |

Rent out space in |

Rent out separate |

Rent out both primary residence | |

|

Average |

$1,897 |

$1,287 |

$2,189 |

$2,028 |

|

$0-$999 |

34 % |

55 % |

24 % |

29 % |

|

$1,000-$1,999 |

40 % |

35 % |

44 % |

38 % |

|

$2,000-$2,999 |

15 % |

7 % |

19 % |

18 % |

|

$3,000+ |

10 % |

5 % |

14 % |

14 % |

About the CIBC Landlord Poll: On March 2nd and May 4th, an online survey was conducted in two parts among a total of 3,023 randomly selected Canadian adults. From April 5th to April 13th 2018, a second online survey was conducted among 2,153 Canadian adults who own at least one property and use at least a portion of it for rental income. All those interviewed are Angus Reid Forum panellists. The margin of error—which measures sampling variability— is +/- 2.5%, 19 times out of 20. Discrepancies in or between totals are due to rounding.

About CIBC

CIBC is a leading Canadian-based global financial institution with 11 million personal banking, business, public sector and institutional clients. Across Personal and Small Business Banking, Commercial Banking and Wealth Management, and Capital Markets businesses, CIBC offers a full range of advice, solutions and services through its leading digital banking network, and locations across Canada, in the United States and around the world. Ongoing news releases and more information about CIBC can be found at www.cibc.com/en/about-cibc/media-centre.html or by following on LinkedIn (www.linkedin.com/company/cibc), Twitter @CIBC, Facebook (www.facebook.com/CIBC) and Instagram @CIBCNow.

SOURCE CIBC - Consumer Research and Advice