{kind=link}

Using points to reach financial goals sooner is often overlooked, as are the potential tax implications of some redemptions, says CIBC's Jamie Golombek

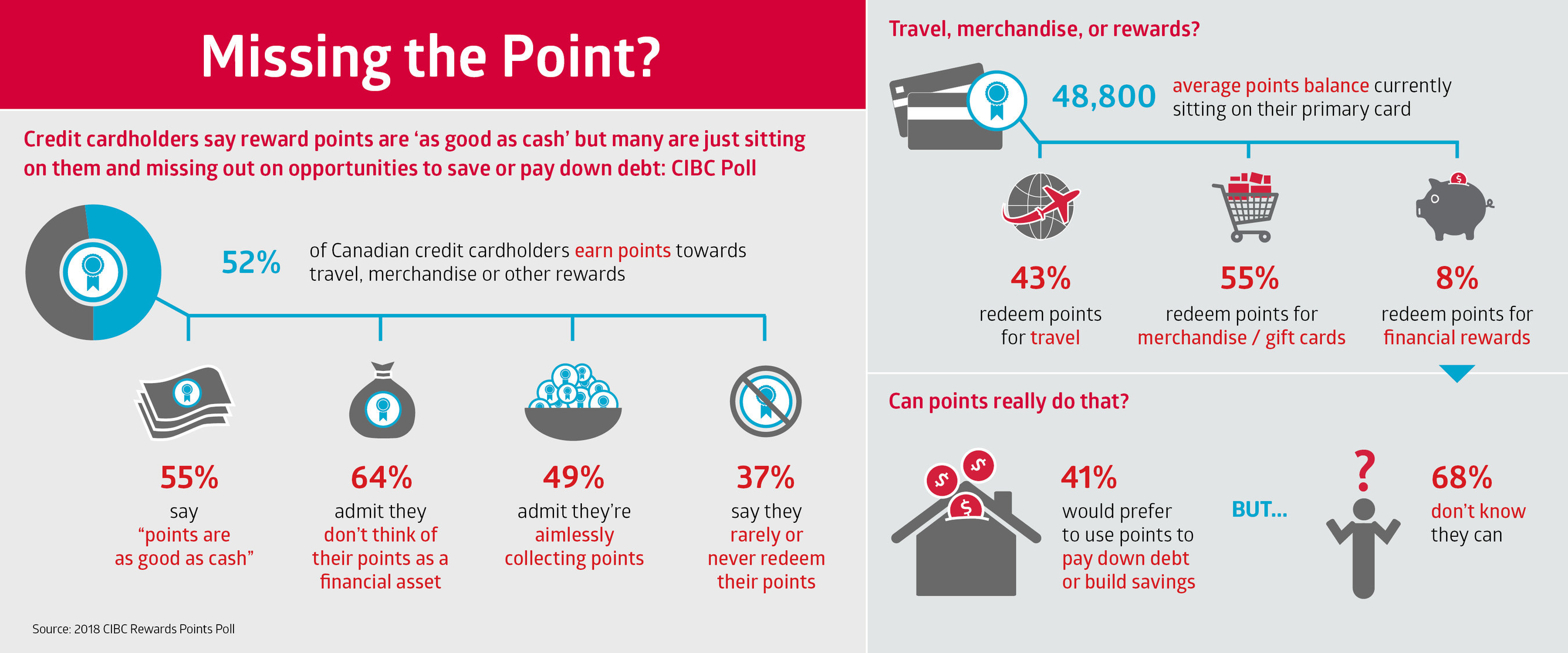

TORONTO, June 28, 2018 /CNW/ - CIBC (CM:TSX) (CM:NYSE) -- A new CIBC poll finds that Canadians who earn reward points on their credit card say points are 'as good as cash', yet most (64 per cent) don't think of them as a financial asset and risk missing opportunities to save money or pay down debt. About half (49 per cent) admit they're aimlessly collecting points, and two in five (37 per cent) say they rarely or never redeem their points.

")

"Canadians say reward points are as good as cash, but many aren't spending them to realize that value," says Jamie Golombek, Managing Director, Tax & Estate Planning, CIBC Financial Planning and Advice. "It's important to think of your points as any other asset, and use them to achieve a financial goal – whether that's to help with the cost of a dream vacation, purchase an item you'd otherwise buy with cash, or possibly reduce your debt or boost your savings."

"If you're aiming to pay down debt but you're also planning to take the family away this summer, using points to cover that trip can make a lot of sense," he adds. "But with high debt loads and the potential for higher interest rates, using points towards paying down debt or building savings may also be a good option for some. These lesser known financial opportunities that many cards offer can often get overlooked if you're socking away points without a plan to spend them or aren't sure what redemption options are available to you."

The poll also reveals that, on average, cardholders are sitting on 48,800 points on their primary credit card – enough for two short-haul flights for a weekend getaway or a new BBQ or garden trimmer this summer, depending on the loyalty program. These points may also translate to a contribution of up to $400 towards the balance of your credit card, mortgage or line of credit, or up to $400 towards a registered plan such as a TFSA, RRSP or RESP – widely available redemption options that most cardholders (68 per cent) don't believe or aren't sure are available to them.

Moreover, when it comes to understanding the value of their points, the majority of reward cardholders (73 per cent) admit that they don't actually check or compare the retail cost of purchasing an item or trip before redeeming points for it. Nor do they compare various redemption options to determine the best value for their points (71 per cent).

"It's important to know what your points are worth, both in terms of their retail or fair-market value, as well as how different redemption options compare, so you can get the biggest bang for your buck in the context of your overall goals," says Mr. Golombek. "You may even put more money in your pocket when you factor in the additional tax advantages of investing in a registered plan like a TFSA or RRSP, or the extra 20 per cent government grant for education savings in the case of an RESP."

Among those who use their rewards card as their primary credit card, two in five (38 per cent) claim they're saving up points for a big ticket item or a dream vacation. Almost half (49 per cent) admit they're aimlessly collecting points to 'see them pile up', or at most, to occasionally window-shop the rewards catalogue for redemption options. Few (13 per cent) redeem points regularly for items they'd otherwise buy with cash.

"Saving up your points for a planned vacation or item is a great way to offset that expense. But if you're simply piling up points, you may overlook rewards options that you could realize today to give you immediate value or get you further ahead," adds Mr. Golombek.

When it's business, not personal

In a new report Missing the Point?! Financial & tax considerations of loyalty point redemptions, Mr. Golombek and Debbie Pearl-Weinberg, Executive Director, Tax & Estate Planning, CIBC Financial Planning and Advice, outline some of the financial considerations for redeeming points for rewards.

"While loyalty points or rewards earned through personal spending are generally tax-free, things can get a bit tricky for points earned through business spending including travel," says Mr. Golombek.

For example, the redemption of points earned through business expenditures may, in some cases, give rise to a taxable benefit to an employee who later uses those points for personal benefit. According to Canada Revenue Agency, the fair market value of that reward must be reported as remuneration or income to the employee if the points are converted to cash, the plan is considered to be an alternate form of remuneration, or the plan is for the purpose of tax avoidance. The same principles should generally apply to a business owner who redeems points collected on a business credit card for personal benefit, such as tickets for a family vacation.

Other considerations

Some additional tax considerations include donating points to a registered charity, or using points for medical travel which may entitle you to claim a medical expense credit, adds Mr. Golombek. The tax implications of these considerations, and more, are discussed in the report.

Key poll findings:

- 52 per cent of Canadian credit cardholders earn points towards travel, merchandise or other rewards

- Nearly half of those (47 per cent) use their rewards point card as their primary credit card for everyday purchases:

- 48,800 is the average points balance currently sitting on their primary card

- 1 in 5 (20 per cent) don't know how many points they've accumulated on their card

- Top redemption choices are travel (43 per cent) and merchandise (37 per cent)

- 37 per cent rarely or never redeem their points

- 55 per cent say "points are as good as cash," yet 64 per cent admit they don't think of their points as a financial asset

- 68 per cent of respondents don't believe or aren't sure they can use their points to pay down debt or contribute to savings, yet 41 per cent would prefer these options over redeeming for non-essentials like merchandise

About the CIBC Rewards Points Poll: On June 13, 2018 an online survey of 1514 randomly selected Canadian adults who are Maru Voice Canada panelists was executed by Maru/Blue. For comparison purposes, a probability sample of this size has an estimated margin of error (which measures sampling variability) of +/- 2.5%, 19 times out of 20. The results have been weighted by education, age, gender and region (and in Quebec, language) to match the population, according to Census data. This is to ensure the sample is representative of the entire adult population of Canada. Discrepancies in or between totals are due to rounding.

About CIBC

CIBC is a leading Canadian-based global financial institution with 11 million personal banking, business, public sector and institutional clients. Across Personal and Small Business Banking, Commercial Banking and Wealth Management, and Capital Markets businesses, CIBC offers a full range of advice, solutions and services through its leading digital banking network, and locations across Canada, in the United States and around the world. Ongoing news releases and more information about CIBC can be found at www.cibc.com/en/about-cibc/media-centre.html or by following on LinkedIn (www.linkedin.com/company/cibc), Twitter @CIBC, Facebook (www.facebook.com/CIBC) and Instagram @CIBCNow.

SOURCE CIBC - Consumer Research and Advice