{kind=link}

Women are three times more likely than men to quit work to care for loved ones, and others reduce hours or give up career advancement

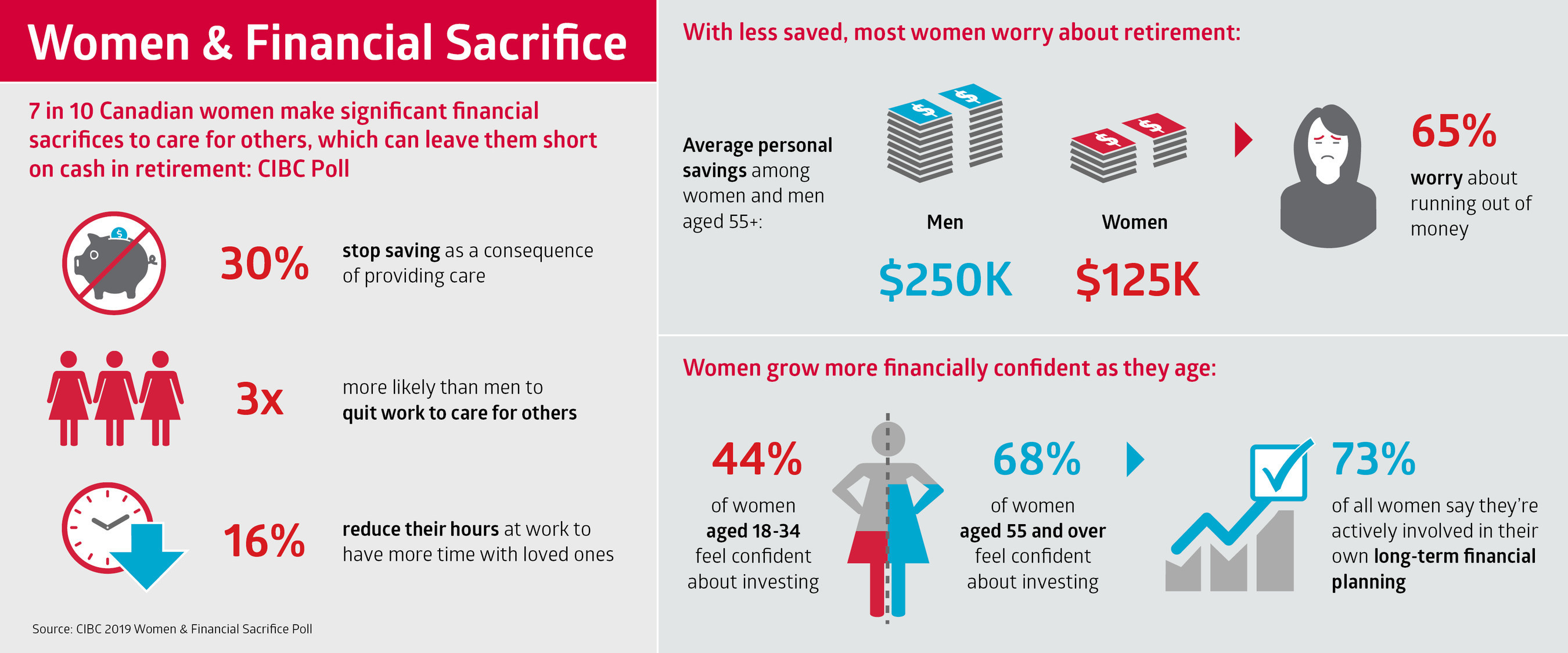

TORONTO, Feb. 21, 2019 /CNW/ - As many as seven in 10 (69 per cent) Canadian women make significant financial sacrifices including putting their careers on hold to care for loved ones, which can put them at a considerable disadvantage to men when it comes to saving for their retirement, a new CIBC study finds. In fact, almost 1 in 3 (30 per cent) women say they've reduced or stopped saving as a direct consequence of childcare or eldercare responsibilities.

")

But, whether by necessity or choice, women aren't shying away from participating in what happens to their money: three-quarters (73 per cent) say they're actively involved in their own long-term financial planning – a number that grows higher the older they get, rising to 82 per cent among women aged 55+.

"Women take on the bulk of care responsibilities for children and aging loved ones. However, it's encouraging to see that despite the pull of family duties, women are jumping into the driver's seat when it comes to their own financial well-being," says Kathleen Woodard, Senior Vice President, CIBC Imperial Service in a new video. "Making the decision to quit working, reduce hours or forgo career advancement can have a direct impact on savings, so it's critical to put a plan in place and take steps to address any savings shortfall to ensure their own financial security down the road."

Key poll findings:

- Almost 3 in 5 (57 per cent) women say there have been consequences to their career after caring for others, compared to 45 per cent of men

- 1 in 5 (19 per cent) have taken an extended absence and an almost equal number have decreased work hours (16 per cent)

- Women are nearly three times more likely than men to quit work to provide care at 16 per cent, compared to 6 per cent of men

- 18 per cent hesitated on making a career move

- Nearly a third (30 per cent) of women have reduced or stopped contributing to savings as a consequence of caring for others

- On average, women aged 55+ have amassed approximately $125,000 in personal savings – half of what men have saved at $250,000

- 83 per cent of women are willing to make personal sacrifices to save more money

- 65 per cent of women worry about running out of money in retirement

- On a positive note, 90 per cent of women are the main or co-decision maker when it comes to investing

According to Statistics Canada, women can expect to live approximately four years longer than men so therefore have to finance a longer period of retirement. This, coupled with the fact that more women put their careers on hold, means women may need to adopt different strategies for retirement planning.

"If you intend to take some time to provide care for a loved one, consider how you might split care responsibilities to reduce the economic impact on one caregiver and take advantage of dual employer benefits," says Ms. Woodard. "Ramping up on RRSP contributions before your planned time-off or having a spouse contribute to your own retirement savings during the break can also help make up for the lost income," she adds.

The double hit: Caring for aging loved ones also impacts savings

The financial challenges of caring for others are not limited to young mothers: caring for sick or aging loved ones can often boomerang later in life just as women's careers are taking off and their income and ability to save more money increases. In fact, 42 per cent of women aged 55-64 are already responsible for the care of aging parents – a cost estimated at $33 billion a year in out-of-pocket expenses and time off work on a national basis, with the largest impact falling to women, according to a recent CIBC report.

"You may make a deliberate choice to take time off to care for kids and plan for it accordingly, but more often than not, we don't plan for unexpected curveballs that can affect our loved ones' physical or mental health and can impact any plans to catch up on savings," says Ms. Woodard. "Your best bet is to plan ahead and take steps now to help you weather uncertainty later on."

How you save matters – Invest early, invest often

While women say they have a good handle on saving money (94 per cent), household budgeting (93 per cent), and debt management (87 per cent), almost half (46 per cent) admit they lack confidence when it comes to investing. As a result some may not be making the most of the money they save.

The study shows that women tend to invest more conservatively than men, favouring guaranteed investments for fear of losing money (43 per cent compared to 35 per cent). And, most (76 per cent) say they'd opt for lower risk to preserve capital rather than take a higher risk for the chance of greater returns, compared to 62 per cent of men who would make the same choice.

"It's not only how much you save, but how you're saving it that matters. Every little bit adds up, especially when you have more time to save," says Ms. Woodard. "Investing early and regularly in a well-balanced and diversified portfolio with the potential for higher returns can get you on the right financial track and help ensure you don't miss out on years of contributions, earnings potential and compound interest."

The study reveals that women's investing know-how increases as they age, growing from 44 per cent among those aged 18-34 to 68 per cent among those aged 55+, with widows showing more investor confidence than any other group male or female. What's more, women aren't standing still: 79 per cent have taken action over the past year to empower themselves and grow their confidence, especially among younger women aged 18-34. Perhaps not surprisingly, women are also more likely than men to ask for directions and seek expert advice when investing (68 per cent compared to 59 per cent).

Tips to help you care for others and yourself:

- Consider splitting care responsibilities with a spouse or other relative to level any career impact on a single care-giver and take advantage of multiple employer benefits. If you're providing care for an aging parent or relative, be sure to consider what tax relief/credits may be available to you to offset costs.

- Save (even when you think you can't) by ramping up RRSP contributions prior to your work-leave or having a spouse contribute to retirement savings in your name during the time off.

- Invest early, regularly and for the long-term – Work with an advisor to determine your short and long-term goals and set up an investment plan that matches your risk tolerance and achieves your goals.

About the 2019 Women & Financial Sacrifices poll: From November 28th to December 6th 2018 an online survey of 4,591 randomly selected Canadian adults who are Maru Voice Canada panelists was executed by Maru/Blue. For comparison purposes, a probability sample of this size has an estimated margin of error (which measures sampling variability) of +/- 1.3%, 19 times out of 20. The results have been weighted by education, age, gender and region (and in Quebec, language) to match the population, according to Census data. This is to ensure the sample is representative of the entire adult population of Canada. Discrepancies in or between totals are due to rounding.

About CIBC

CIBC is a leading North American financial institution with 10 million personal banking, business, public sector and institutional clients. Across Personal and Small Business Banking, Commercial Banking and Wealth Management, and Capital Markets businesses, CIBC offers a full range of advice, solutions and services through its leading digital banking network, and locations across Canada, in the United States and around the world. Ongoing news releases and more information about CIBC can be found at www.cibc.com/ca/media-centre or by following on LinkedIn (www.linkedin.com/company/cibc), Twitter @CIBC, Facebook (www.facebook.com/CIBC) and Instagram @CIBCNow.

SOURCE CIBC - Consumer Research and Advice